The AI Capex Debate: Misallocation or Generational ROIC?

Wall Street thinks Big Tech may be lighting $700 billion a year on fire.

If that’s true, we’re in the early innings of the biggest capital misallocation since 1999.

If not, we’re looking at one of the greatest ROIC expansions in modern corporate history.

Collectively, the five largest hyperscalers – Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), Meta (META), and Oracle (ORCL) – are spending roughly $710 billion on AI-related capital expenditures this year. That’s basically $2 billion per day flowing toward compute, data centers, fiber, energy, and cooling systems for machines that most people only interact with via chatbox.

That’s why the kneejerk reaction to that staggering number is some version of: “That seems like way too much,” with many questioning whether this is the greatest capital misallocation since the dot-com bubble.

Here’s the thing though: when you actually sit down and do the math – properly, with realistic assumptions about revenue, margins, and timelines – the spending looks more than defensible. It looks potentially brilliant.

If so, the current choppiness in AI-related equities may turn out to be one of the more attractive entry points investors will see in this cycle.

Let’s walk through the numbers. No hype – just napkin math, done carefully.

The Three Revenue Engines Powering AI Capex

Before you decide whether $700 billion is reckless or rational, you need to understand what that capital is actually buying.

At full maturity, the AI business model has three distinct revenue engines, each with different economics and timelines.

Consumer AI Subscriptions: The Base Layer of AI Revenue

This is the simplest vector to understand because it’s already happening. ChatGPT Plus, Claude Pro, Gemini Advanced – each of these frontier models is available to folks like you and me for $20- to $30-per-month subscriptions.

This is the consumer market. It is undeniable and already scaling. The question is how large it gets.

There are roughly 5.5 billion smartphone users globally. Subtract the 2 billion or so who live below any viable income threshold for a $20/month software subscription, and you have roughly 3.5 billion addressable consumers. Assume tiered global pricing – $25/month in the U.S. and developed markets, $12 in Europe and South America, $4 in price-sensitive emerging markets, with penetration rates of 50%, 20%, and 5% respectively – and you arrive at roughly 625 million global subscribers generating a blended ARPU of about $16/month.

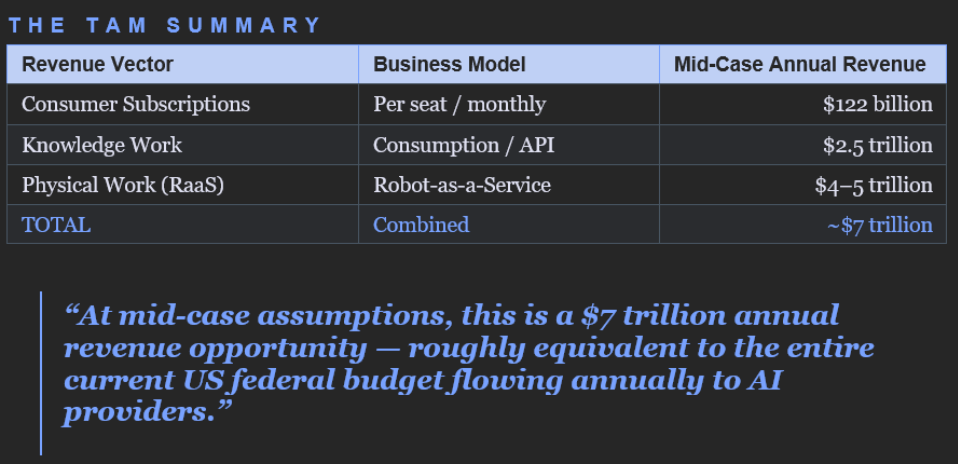

Annual consumer revenue at full penetration: approximately $120 billion. Real money, but in the context of what follows, almost a rounding error.

Enterprise AI and Knowledge Work Automation

This is where the numbers start becoming genuinely disruptive for people working in knowledge-intensive industries.

There are approximately 560 million “knowledge workers” globally – i.e. lawyers, analysts, engineers, accountants, marketers, consultants, etc. Their all-in yearly pay averages roughly $58,000 globally (skewed by the $80K-plus developed-market average against cheaper emerging-market equivalents), implying a total global knowledge work labor cost of approximately $32 trillion per year.

Under a consumption-based pricing model – where enterprises pay for AI based on value delivered rather than seats occupied – vendors can price against labor savings rather than software budgets. If AI ultimately automates 40% of knowledge work at scale (a reasonable mid-case), and vendors capture 20% of that value (consistent with historical enterprise software economics), the math looks like this:

$32 trillion × 40% automation × 20% capture rate = $2.56 trillion in annual revenue.

The range is wide – conservative assumptions based on this formula yield roughly $1 trillion, while a bull case approaches $5 trillion. But even the conservative case is transformational.

The important structural point is that this pricing model anchors against labor costs, not software budgets. Those are 10- to 50x different in scale, which is why the transition from per-seat to consumption pricing is the single most important business model evolution to watch in enterprise AI.

Physical AI and Robotics: The Next Multi-Trillion-Dollar Market

If the knowledge work numbers made you pause, the physical labor numbers will leave you stunned.

There are approximately 3 billion physical workers globally – in manufacturing, construction, agriculture, logistics, warehousing, transportation, food service, and healthcare delivery. Their all-in yearly pay averages roughly $13,000 globally (blending $45K developed-market workers with $8K developing-market workers), implying a total global physical labor cost of approximately $39 trillion annually. That’s larger than the knowledge work cohort.

Up to this point, we’ve been talking about software replacing thought. The next phase is software directing motion.

Physical AI means models that don’t just generate text – they control machines, becoming the “brains” of robots. Robot-as-a-Service – where vendors lease the integrated hardware/software system rather than sell it outright – is already the emerging commercial model, as shown by Figure AI‘s deals with BMW, Amazon’s warehouse robotics buildout, and Tesla‘s (TSLA) Optimus program.

We are in the early innings of what becomes a $4- to $5 trillion annual revenue stream at maturity, assuming realistic penetration of roughly 40% of automatable physical work over 20 years.

This vertical has a different gating factor than the others. It’s less about core model capability – which is advancing rapidly – and more about hardware cost curves. Humanoid robots need to reach roughly $15- to $20,000 per unit for the economics to work broadly. Currently, they’re at $20- to $30,000 and falling. History suggests hardware cost curves are not to be bet against.

For example, industrial robot arms cost over $100,000 in the early 2000s; today, collaborative bots from companies like Universal Robots can be deployed for under $30,000.

Solar module costs have fallen more than 90% over the past two decades. Lithium-ion battery costs have dropped nearly 85% since 2010.

Hardware cost curves compound faster than most analysts model.

AI Total Addressable Market: A $7 Trillion Opportunity

Now, if we combine our estimates for each of these three revenue vectors…

We arrive at a more conservative annual total of $7 trillion – nearly 10x what hyperscalers will spend on AI-related capex this year.

Let’s Talk AI Margins…

Yet, revenue is only half the story. What matters to investors is profit. And AI businesses – like all businesses – have costs. So, let’s be realistic about margins across those three vectors.

Consumer AI is largely a software business at scale. Inference costs are falling roughly 10x every 12 to 18 months as hardware improves and efficiency compounds. At maturity, consumer AI margins should converge toward that of mature software economics, around 50- to 60% operating margins. This is where Microsoft Azure runs and roughly where Google’s mature products operate.

Knowledge work enterprise AI sits at 35- to 45%: higher compute costs than the consumer vector (because complex enterprise queries run longer) but still a software business without major physical cost structures.

Physical work/RaaS is structurally different. Robots depreciate, require maintenance, consume energy, and need field service teams. This looks more like an industrial leasing business at 20- to 30% operating margins – still strong but not like software.

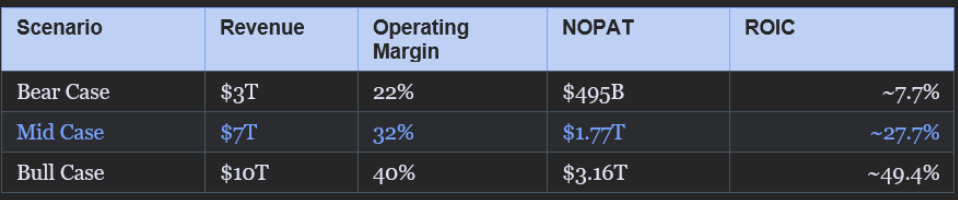

Blended across the $7 trillion revenue base (weighted heavily toward the physical work vertical which dominates at maturity): approximately 32% operating margin. Apply a 21% corporate tax rate, and you arrive at roughly $1.77 trillion in annual after-tax operating profit at full maturity.

For context, the entire S&P 500 currently generates roughly $1.5 trillion in annual after-tax earnings. The AI stack, at maturity, could generate more than that – perhaps concentrated among just a handful of companies.

Calculating the ROIC On AI Capex

So, let’s do what the market keeps threatening to do but rarely finishes: calculate the return on invested capital.

If capex stays at $700 billion per year for 20 years, gross cumulative spend is $14 trillion. Approximately 55- to 60% of that is maintenance capex – replacing GPUs that become obsolete every few years, refreshing networking equipment, upgrading cooling systems. Net new invested capital added over 20 years, then, is roughly $5.9 trillion. Adding the existing infrastructure base of approximately $500 billion, total cumulative net invested capital reaches approximately $6.4 trillion.

ROIC at maturity: $1.77 trillion Net Operating Profit After Tax (NOPAT) / $6.4 trillion invested capital = approximately 27- to 28%.

To put that in context, Google runs around 25- to 30% ROIC at maturity. Microsoft is in the 35- to 40% range. Apple (AAPL), the best large-cap ROIC story of the last two decades, runs 50- to 55%. Therefore, a 28% ROIC on a $6.4 trillion invested capital base – generating $1.77 trillion in annual profit – is not reckless speculation. It’s in the range of the greatest capital allocation stories in the history of American business.

Now, the bear case – 7.7% ROIC – is genuinely bad; barely above cost of capital. But it requires revenues to come in at less than half the mid-case, margins to compress significantly due to competition, and tax rates to rise. That’s a plausible bad scenario, though not a base case.

And then you have the bull case, with nearly 50% ROIC, which we think is actually very possible and far more likely than the bear case. At that level, Big Tech could easily justify spending $1 trillion-plus per year on AI capex over the coming decades.

The AI Capex J-Curve and Why Short-Term Returns Look Ugly

Here’s the catch that explains all the market anxiety. ROIC at maturity is not ROIC today.

When you spend $700 billion in year one against revenues still in the low hundreds of billions, your interim returns look terrible. The J-curve is real, and it’s deep.

By rough estimate, ROIC doesn’t cross a 12% cost-of-capital threshold until around year nine or 10. For several years, the industry will be consuming capital faster than it’s returning it. That’s the funding gap. We’re already seeing it surface in private credit vehicles funding AI infrastructure – Blue Owl‘s (OWL) recent redemption pressures are an early preview. And every time revenue growth wobbles, public markets price that same fear into AI infrastructure stocks.

But here’s the key distinction: the companies most exposed to J-curve pain are those financing AI infrastructure with expensive short-duration capital: private credit borrowers without existing cash flow cushions.

The hyperscalers themselves are a completely different story. Microsoft generates $90-plus billion in free cash flow annually from its existing businesses. Amazon has AWS. Alphabet has Search. Meta has advertising. These companies can fund the J-curve out of operating cash flow, without dilution or distress, essentially indefinitely.

The J-curve that destroys over-levered, pure-play infrastructure borrowers is merely uncomfortable for the hyperscalers. Their existing businesses print the cash to fund it.

The AGI Variable: Why AI Capex May Be Understated

Everything we’ve discussed so far has been built on relatively conservative assumptions about AI capability – that models improve gradually, automate a meaningful but bounded fraction of knowledge and physical work, and compete in a market with rational pricing dynamics.

None of those assumptions hold if artificial general intelligence (AGI) arrives within the decade. And it would be dishonest not to note that the pace of capability improvement this year alone has been genuinely startling.

Consider what has happened in just the past few months: ChatGPT 5.2 to Gemini 3.0 to Claude 4.6 to Gemini 3.1, each representing leapfrog improvements over its predecessor in reasoning, coding, multimodal understanding, and agentic capability. These are not incremental dot releases. Each new frontier model is doing things that were considered firmly out of reach 12 months prior.

If the current trajectory continues – and there is no clear evidence yet of a scaling plateau – AGI-class systems (models that can perform virtually any cognitive task at human level or above) are a plausible outcome within five to 10 years. Most serious researchers now put this at somewhere between “sooner than we thought” and “we’re not sure anything can stop it.”

What does AGI do to our $7 trillion TAM estimate? It makes it look like we forgot a zero. Possibly two.

An AGI that can perform any knowledge work task at human expert level – available at inference cost, which is trending toward fractions of a cent per query – is not a productivity tool. It is a replacement for a substantial fraction of all professional services.

Global professional and business services alone represent approximately $15 trillion in annual spend. Legal, accounting, consulting, finance, software development, research: all of it becomes addressable.

The physical dimension is equally staggering. An AGI directing a humanoid robot isn’t cornered into being a warehouse picker. It could be a surgeon, a foreman, a teacher, a nurse. The TAM expands into domains currently considered off-limits for automation.

The $700 billion in annual capex, viewed through an AGI lens, isn’t aggressive. It’s table stakes. And the companies that have the compute infrastructure in place when AGI arrives – regardless of near-term ROIC – will be in an incomparably superior competitive position to those that tried to be capital-efficient in 2025 and ’26.

This is why hyperscaler CEOs sound almost bored when analysts ask them to justify the capex. They’re not running a standard IRR model. They’re buying an option on a discontinuity that would make any IRR model obsolete.

The Geopolitical Dimension of AI Infrastructure Spending

There is one more dimension to this analysis that pure financial modeling cannot fully capture: geopolitics.

China is not watching American AI development with passive interest. It is running a coordinated national effort, backed by state resources, to achieve AI parity or superiority. DeepSeek’s R1 model – which achieved near-frontier performance on several public benchmarks at a fraction of the compute cost – was a genuine wake-up call. Not because it proved American AI was losing, but because it demonstrated that the gap is narrower than comfortable and that a determined adversary with enormous engineering talent can move faster than expected.

That reframed AI competition not just as a commercial race but as a strategic one.

When you frame AI leadership as a matter of national security and economic sovereignty – which it plainly is – the ROIC calculus changes.

In other words, at some level of strategic importance, the question stops being “what’s the IRR?” and becomes “what’s the cost of losing?”

The strategic cost of falling materially behind in AI capability would extend beyond corporate earnings – affecting defense systems, economic competitiveness, and technological standards-setting power.

This doesn’t mean capex discipline is irrelevant. Wasted capital is still wasted capital. But it does mean that the “what if the market isn’t there yet?” risk needs to be weighed against the “what if we show up to the AGI moment without enough compute?” risk. For the hyperscalers, the latter appears to be the more frightening scenario.

Putting the AI Capex Debate In Perspective

Let’s summarize.

At mid-case assumptions – $7 trillion in annual revenue, 32% blended operating margins, $6.4 trillion in cumulative net invested capital – the ROIC on AI infrastructure is approximately 28%. That’s best-in-class for any large industry in history. The bull case, at $10 trillion revenue and 40% margins, implies ~49% ROIC. Apple-tier. Exceptional.

The bear case – ~8% ROIC – is bad but survivable for companies with existing profitable businesses subsidizing the buildout. It is not survivable for over-levered pure-play infrastructure borrowers. This distinction matters enormously for how you position across the AI supply chain.

The J-curve means that periodically, the next three to five years will look ugly from a returns perspective. Revenue will grow fast but not fast enough to justify $700 billion in annual spend on a year-by-year basis. Markets will use these moments to panic. Blue Owl’s redemption halt is a preview of the periodic liquidity scares that will punctuate the next few years as private credit funding AI infrastructure encounters the J-curve in real time.

AGI optionality is unpriced and unmodeled. If you believe – as the pace of model improvement in the past six months alone suggests – that AGI-class systems arrive within a decade, then every conservative estimate in this analysis is drastically understated, and current capex budgets should arguably be higher, not lower. The hyperscalers almost certainly believe this, which is why their capex guidance goes up every quarter regardless of market reaction.

And the geopolitical dimension means that even a negative net present value (NPV) scenario doesn’t necessarily argue for cutting back. Nations and companies at the frontier of AI development hold a form of strategic leverage that transcends normal financial optimization.

For investors, the practical read is this: the current choppiness in AI supply chain stocks – the GPU manufacturers, data center REITs, power infrastructure providers, networking companies, and the hyperscalers themselves – reflects legitimate short-term anxiety about J-curve dynamics and a slowing of the most euphoric capex expectations.

It does not reflect a fundamental challenge to the underlying economic logic.

Where This Leaves Investors

The math suggests:

- AI capex at $700 billion per year is defensible.

- Capex rising toward $1 trillion per year over the next decade is also defensible.

- The companies building this infrastructure – and doing it with the balance sheet strength to survive the J-curve – are positioning themselves for one of the most extraordinary returns on invested capital in the history of industrial capitalism.

Blue Owl’s stress is a reminder that capital structure matters. Over-levered borrowers will feel the J-curve. Cash-rich hyperscalers won’t.

The companies with fortress balance sheets are building toward a 20-year ROIC profile. The market is judging them on a two-year earnings window.

That disconnect won’t last forever; which means this is an opportunity worth taking seriously.

And there’s one more layer to this story.

In every technological revolution, the early money goes to infrastructure. The real money goes to the platform that sits on top of it.

During the internet buildout, Cisco (CSCO) and Intel (INTC) ran first. Then came Google, Facebook, Netflix (NFLX) – and the gains were exponentially larger.

If AI follows that same pattern, the next shift won’t be into chips or data centers. It will be into the AI platform itself.

I’ve identified a way for everyday investors to stake a claim in what could become the first pure-play AI platform company – before its expected IPO, and for less than $10.

When this company goes public later this year – potentially at a valuation approaching $1 trillion – the index inclusion effect alone could create a massive second wave of demand.

The infrastructure buildout is stage one. The platform capture is stage two.

And stage two is where fortunes are made.