The Quantum Computing Paradox: Brilliant Future, Complicated Present

There is a number buried in a Google research paper from late 2024 that raised the ceiling on what computers can do.

A benchmark calculation completed by Google’s Willow quantum chip in roughly five minutes would take the world’s fastest classical supercomputer an estimated 10 septillion years. That’s 10 followed by 24 zeros. The universe is only 13.8 billion years old.

That number describes a fundamental shift in what computers can do – and by extension, what becomes possible in medicine, finance, defense, logistics, and artificial intelligence.

The Quantum Computing Market Opportunity Is Massive

How big is the quantum computing market? Estimates vary depending on who’s doing the math, but the broad consensus from serious research firms is that this is a multi-hundred-billion-dollar industry in the making.

McKinsey projects quantum technologies could generate up to $97 billion in annual global revenue by 2035, with computing accounting for the lion’s share at $72 billion.

Boston Consulting Group puts the addressable market for quantum hardware, software, and services at up to $170 billion by 2040.

Jefferies, taking the widest view, sees the total addressable market approaching $198 billion by the same year.

The verticals driving this demand are enormous:

- Pharmaceutical companies that could slash drug development timelines from a decade to months

- Financial institutions running risk models and portfolio optimization at unprecedented speed

- Defense contractors simulating complex battlefield scenarios in real time

- Energy companies optimizing power grids

- Logistics firms solving routing problems that currently require armies of operations researchers

There is no major industry that won’t be fundamentally disrupted if quantum computing delivers on its promise.

The question has never been whether these systems work; it’s whether we can make them reliable enough to matter commercially.

And that answer, as we’ll get to shortly, is more complicated than the cheerleaders would have you believe.

Top Quantum Computing Companies Leading the Race

The most direct ways to invest in the quantum computing revolution are the pure-play public companies — the ones where quantum isn’t a side project but the entire business:

IonQ: The Revenue Leader In Quantum Computing

Using trapped-ion technology — barium and ytterbium atoms suspended by lasers as their qubits — IonQ (IONQ) has achieved 99.99% two-qubit gate fidelity, the highest in the industry by a wide margin. It has also expanded beyond quantum computing into networking, sensing, and security – positioning itself as a full-stack quantum platform company. And its pending acquisition of SkyWater Technologies signals serious intent to own the quantum supply chain.

The company generated $130 million in full-year 2025 revenue (up 202% year-over-year) and is expecting $225- to $245 million in FY2026.

D-Wave: The First Commercial Quantum Player

While the rest of the industry debates when quantum computers will do something useful, D-Wave Quantum (QBTS) is already doing it.

Its edge lies in its quantum annealing approach: architecturally distinct from gate-model competitors and uniquely suited for optimization problems, which represent one of the largest near-term commercial opportunities in the space.

According to its latest earnings report, “During FY2025, D-Wave recognized revenue from over 135 individual customers encompassing over 70 commercial enterprises, including over two dozen Forbes Global 2000 companies.” Those are paying customers running production workloads across logistics, defense, telecom, manufacturing, and finance – right now.

With a $20-million system sale to Florida Atlantic University, a $10-million Fortune 100 enterprise license, and a 1,500% pipeline expansion planned for 2026, D-Wave is pulling away from the pack in terms of commercial traction.

Rigetti: A Long-Term Quantum Bet

Rigetti Computing (RGTI) is the only pure-play quantum company that controls its own chip fabrication — and the only one whose CEO will tell you plainly when the technology will actually matter.

On the company’s Q4 2025 earnings call, CEO Subodh Kulkarni told investors directly that true quantum advantage is ‘roughly three years away’ — a refreshingly candid admission in an industry that rarely acknowledges inconvenient timelines.

Rigetti’s differentiator is its chiplet architecture and custom quantum fab (Fab-1), which gives it hardware roadmap control that no other pure-play public company has.

Rigetti is targeting a 1,000-plus qubit system by the end of 2027 with 99.8% gate fidelity – meaning fewer than one in 500 quantum operations produces an error, a threshold widely considered necessary for running the complex, real-world calculations that justify commercial deployment. With $590 million in cash and no debt, it has the runway to execute.

Rigetti’s CEO will be the first to tell you this is a 2028-29 investment story. That honesty is, paradoxically, one of the more bullish things about the company.

Big Tech’s Quantum Computing Push

The pure-plays are building the future. But the incumbents have the capital, the talent, and the infrastructure to define it.

IBM (IBM) has the most aggressive quantum roadmap of any large company, targeting verified quantum advantage by the end of 2026 and a fault-tolerant quantum computer by 2029.

Alphabet (GOOGL) achieved the landmark ‘below threshold’ error correction with its Willow chip. In other words, adding more qubits now reduces error rates rather than increasing them.

Microsoft (MSFT) is betting on topological qubits with its Majorana 1 chip.

Quantinuum — largely owned by Honeywell (HON) — has arguably the most accurate commercial system available today with its Helios machine.

And Amazon (AMZN) is quietly building quantum cloud infrastructure through its Amazon Braket, giving enterprises a hardware-agnostic on-ramp to quantum without requiring them to bet on a single architecture.

Why Quantum Computing Stocks Exploded In 2024-25

It took one Google chip announcement to turn a decade of quiet laboratory progress into a full-blown market mania. What happened next is a masterclass in how Wall Street prices the future – and what it costs when reality doesn’t move at narrative speed.

The trigger? Google’s December 2024 announcement of the Willow chip. Suddenly, quantum computing went from being considered a future technology to a present reality.

The stock market, which had largely ignored these companies for years, woke up practically overnight. And the moves were extraordinary.

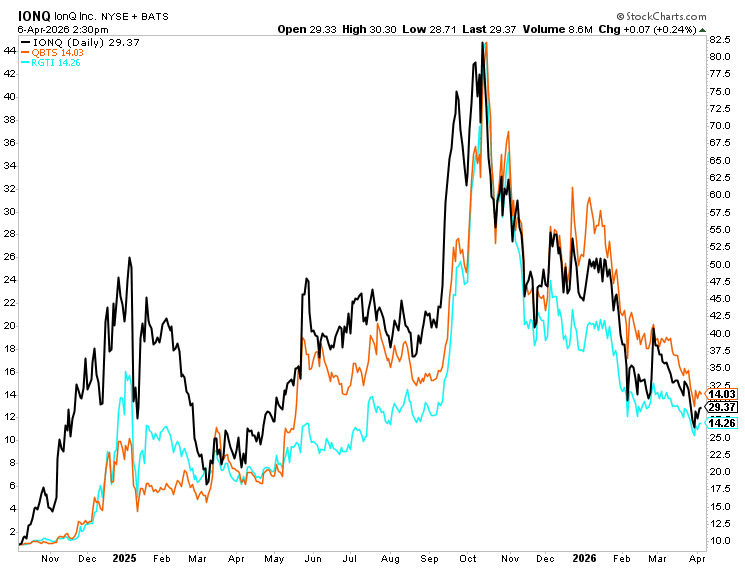

IonQ went from roughly $7 per share in early 2024 to nearly $85 by early 2025 – a roughly 12x move in about a year.

Rigetti went from under $1 to nearly $60, a gain of more than 6,000% from its lows.

D-Wave went from about $1 to over $45.

These were parabolic, meme-stock-style moves driven by the combination of genuine technical progress, narrative momentum, and an investor base that had just watched AI stocks go vertical and was desperately looking for the next wave.

The technology was genuinely advancing. The long-term thesis was compelling – and remains so.

But markets tend to reprice the future instantaneously and then wait, impatiently, for reality to catch up. And in the quantum computing space, reality moves at a much more deliberate pace than Wall Street.

The Crash: When the Reality Check Arrived

The catalyst for the reversal came in October 2025, courtesy of Nvidia (NVDA) CEO Jensen Huang — a man whose opinion on computing matters more to tech investors than almost anyone else.

Huang estimated that practical, widely useful quantum computing was likely still 15 to 30 years away, with 20 years being his central estimate. And the effect on Wall Street was immediate and brutal.

IonQ fell from $85 to under $30. Rigetti collapsed from nearly $60 to under $15. D-Wave dropped from over $45 to under $15.

In a matter of months, those stocks gave back the majority of their extraordinary gains.

The technology was real. The long-term potential was massive. But the near-term commercial reality did not justify the valuations the market had assigned.

The companies’ financials told the story plainly.

IonQ — by far the strongest revenue performer in the group — generated $130 million in 2025 revenue against losses around $500 million.

D-Wave’s full-year 2025 revenue was $24.6 million – alongside losses of $355 million.

And Rigetti’s Q4 revenue was $1.9 million, down 17.4% year-over-year.

Meanwhile, the Willow chip was completing benchmarks that no commercial customer was paying for. Microsoft’s Majorana 1 was a research prototype. IBM’s fault-tolerant roadmap wasn’t nearing the finish; it runs through 2029.

The gap between the narrative and the revenue wasn’t a crack. It was a chasm. Wall Street found it the same way it always does – by falling in.

What Will Drive the Next Rally In Quantum Computing Stocks

Here is the honest truth: quantum computing stocks are not going to sustain a meaningful recovery until they can point to undeniable, large-scale commercial proof that quantum computers are delivering measurable economic value in the real world – not in labs, press releases, or benchmarks, but in production environments where real businesses are paying real money for real results.

The specific catalysts to watch – which are closer than the current stock prices suggest – include:

- Defense contracts at scale. All three of the major pure-play companies we’ve mentioned are actively pursuing U.S. government and defense contracts.

- D-Wave’s missile defense simulation with Anduril and Davidson Technologies showed a 10x improvement in threat mitigation speed.

- IonQ has built out a dedicated federal team pursuing SHIELD program opportunities.

- The Pentagon’s budget is increasing with explicit quantum allocations. A large, named, multi-year defense contract – something in the $50- to $200 million range – would be a sector-wide catalyst that validates both the technology and the business model simultaneously.

- Fortune 500 named customer ROI stories. D-Wave’s CEO described a Fortune 100 company that started with one application, experienced a ‘dramatic improvement in their bottom line,’ and came back asking for an enterprise-wide license. What’s missing is the public naming and quantification of that ROI.

When a marquee company publicly says, ‘we saved $X hundred million using quantum computing on problem Y,’ the sector re-rates. Given the number of enterprise customers already running production workloads, D-Wave is the most likely company to generate this headline in 2026-27.

- National quantum legislation. The National Quantum Initiative Reauthorization Act has bipartisan support in both the House and Senate. Several CEOs called it ‘imminent’ on their Q4 2025 earnings calls. This is essentially the quantum equivalent of the CHIPS Act – a multi-billion dollar federal commitment that unlocks government procurement budgets and institutional credibility for the entire sector. When it passes, expect a meaningful rally across the space.

- IBM’s verified quantum advantage demonstration. IBM has made an explicit public commitment to demonstrate verified quantum advantage by the end of 2026. If it delivers, it won’t just be good news for IBM – it will be a signal flare for the entire industry that the timeline is real and compressing. Every quantum company’s stock should benefit.

The commercial tipping point is coming. When it arrives, these stocks will move fast and hard. The discipline is in waiting for it.

Investment Strategy: When to Buy Quantum Computing Stocks

We want to be unambiguous about where we stand.

The long-term bull thesis on quantum computing is one of the most compelling investment stories of the next decade. This technology will reshape drug discovery, financial modeling, materials science, logistics, cryptography, and artificial intelligence. The companies building it today are laying the foundation for what could be a $100- to $200 billion industry within 15 years.

We are enthusiastic, unapologetically bullish long-term investors in this space. But we are not yet advocates for buying these stocks today.

IonQ at $30, Rigetti at $15, D-Wave at $15 – these are dramatically cheaper than they were at the peak. But ‘cheaper than the top’ is not the same as ‘bottomed out.’ Markets don’t find floors based on long-term theses. They find floors based on near-term catalysts that change the narrative. Without a commercial tipping point, these stocks can drift lower for longer than any bull thesis investor is comfortable with.

The cash burn is real, the timelines are long, and the competition from IBM, Google, and Microsoft is intensifying.

The Bottom Line

The quantum playbook, right now, is straightforward: watch for the commercial catalysts outlined above. When one of those catalysts lands, these stocks will bounce hard.

Let the narrative re-establish itself. Then buy into that momentum with conviction, knowing that the long-term destination is many multiples higher than even the early 2025 peaks.

The future of computing is quantum. The future of the quantum computing trade is patience.

But capital moves toward what can be monetized now.

While quantum is still working toward commercial reality, another shift is already underway – one built on infrastructure that’s already here, scaling and moving capital in real time.

It’s happening at the platform layer.

And historically, that’s where the biggest value accrues. Not at the moment of discovery – but at the point of adoption.

Which leads to a different question…

Where does the capital flowing into AI infrastructure ultimately end up?

One answer is becoming increasingly clear: OpenAI.

Most investors will first encounter it when it goes public – when the story is widely understood and the asymmetry is gone.

We’ve taken a closer look at how that moment could unfold – and how to position before it does.

You can watch the full presentation here.