Opendoor Isn’t a Meme Stock. It’s an AI-Powered Real Estate Disruptor

This kind of setup – hated, heavily shorted, written off by nearly everyone – should sound familiar

Let’s talk about Opendoor (OPEN) stock – because it just staged one of the most furious rallies I’ve seen in my career as a market analyst.

The iBuyer surged from about $0.50 in late June to nearly $5 yesterday. That’s a ~10X gain in less than a month.

Naturally, the financial commentariat has dusted off its favorite lazy takes. It’s a “meme stock,” a “short squeeze” – retail “degenerates chasing garbage.” We’ve heard it all before.

But in all likelihood, they’re probably wrong this time…

Because this doesn’t look like Bed Bath & Beyond (BYON), AMC (AMC), or GameStop (GME) in 2021.

Instead, we think it more closely resembles Carvana (CVNA) in 2023: a heavily shorted, misunderstood, asset-heavy tech disruptor with a vicious cost structure, a brutal macro headwind… and then, suddenly, a pulse.

Could Opendoor stock be next?

Opendoor’s Setup Mirrors Carvana’s Historic Comeback

This kind of setup – hated, heavily shorted, written off by nearly everyone – should sound familiar.

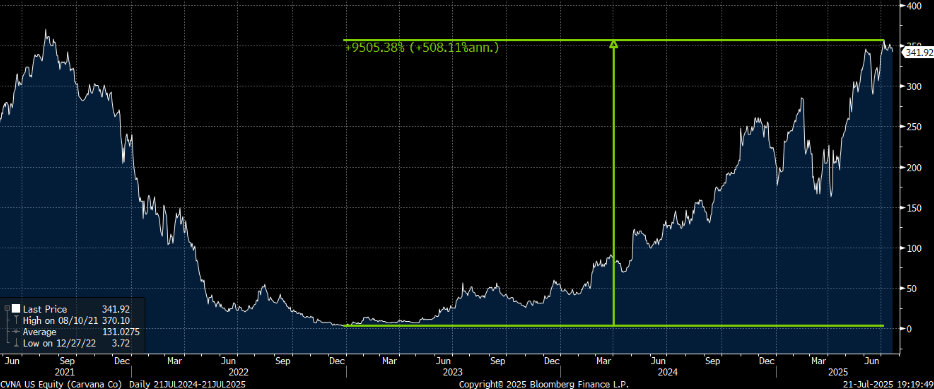

In the inflation/tech crash of 2022, Carvana had been left for dead. Rising rates crushed used car affordability. The company was bleeding cash. Bears gleefully predicted bankruptcy.

And between August 2021 and December 2022, Carvana stock crashed from $370 to under $4 – a 99% stock wipeout.

But then… rates stopped rising. Demand stabilized. Spreads recovered. Operating leverage kicked in.

In the first half of 2023, CVNA soared from $4 to $40… and just kept going… all the way to over $350, for a jaw-dropping 9,500% return in 2.5 years.

Just like that, Carvana exploded off the mat, ripping from $4 to $350-plus in less than three years. Turns out that when you build a massive fixed-cost platform and survive the downcycle, the upside gets spicy.

Now take that exact same blueprint and swap out cars for houses.

Opendoor = The Carvana of Houses

Opendoor and Carvana aren’t just similar; they’re basically the same business model in different clothes.

Both are vertically integrated platforms built to buy, hold, and resell physical assets at scale.

Both try to use software, data, and logistics to eliminate friction in a traditionally painful purchase experience.

And both rely on tight spreads, fast turnover, and massive volume to make the model work.

The difference? The housing market is slower, more expensive, and way more rate-sensitive… Which meant Opendoor got obliterated even harder than Carvana when the macro rug was pulled.

Throughout 2022 and ‘23, mortgage rates doubled. Homebuyers vanished. Inventory sat. Spreads went negative. Opendoor was stuck holding billions in depreciating inventory.

The stock reflected that brutal reality. It fell 99%, just like Carvana. And, just like Carvana, most wrote it off as a terminally broken business model.

But in the rubble, the bones of something better were still there.

From Real Estate Crash Victim to Leaner, Smarter Operator

Here’s what Opendoor quietly did over the past 18 months:

- Slashed inventory to preserve capital

- Tightened its buybox to reduce risk

- Streamlined operations to decrease cash burn

- Focused on high-confidence flips instead of chasing growth

- Launched new product layers like financing and exclusives

In other words, it survived and learned to be better.

Now the tide is turning.

Assuming inflation eases and the Fed begins to cut, institutional experts – from Fannie Mae to Barron’s – anticipate that rates will gradually decline from current ~6.7 % to roughly 5.8 % by late ‘26.

Meanwhile, housing inventory is historically tight. According to Realtor.com and Redfin, the number of active home listings remains well below pre-pandemic norms. Homeowners with ultra-low mortgage rates (locked in during 2020–22) are reluctant to sell. Labor shortages, zoning restrictions, and high construction costs continue to cap the pace of new supply.

But all – including stymied consumer demand, especially from millennials who’ve been priced out – are poised to rebound if rates fall, even modestly.

This is the inflection point. The darkest part of the housing cycle may be behind us.

That’s why, in our view, OPEN isn’t a meme play. It’s operating leverage coming back from the dead.

The AI Engine: What Wall Street Is Missing

Now, here’s the part most people still don’t get: Opendoor is not just a house flipper. It’s building an AI-powered platform that makes data-driven pricing and logistics decisions at scale.

Its core engine is the Automated Valuation Model (AVM) – basically a home-pricing AI trained on millions of data points. That engine decides what to buy, when to buy it, how much to spend on renovations, and when to sell.

In other words, Opendoor is building the world’s first autonomous real estate trader.

The more homes it buys and sells, the smarter the system gets. It’s a data flywheel. And that’s what Wall Street still hasn’t figured out: this is a tech company disguised as a bloated housing operation.

Sound familiar? That was Carvana’s story, too. Everyone saw a used car reseller. Yet, under the hood, it was a real-time pricing engine and logistics network. Once the market realized that, the stock went to the moon.

So, if mortgage rates trend lower and housing demand picks up, Opendoor is positioned to:

- Return to significantly positive contribution margin per home

- Reaccelerate volumes off a leaner base

- Leverage its tech stack into more profitable buys

- Layer on higher-margin products (financing, seller tools, listing exclusives)

- Spark an investor narrative shift: from meme-stock trash heap to AI-powered housing platform

It will be messy, of course. This is still a capital-intensive, rate-sensitive, macro-exposed business.

But that’s exactly what makes it so explosive when conditions flip in its favor.

The Real Estate Market Is Shifting – And Opendoor’s Ready

The Opendoor story isn’t one about fair value. It’s about narrative momentum.

Once perspective shifts – from “this company is doomed” to “wait, it’s working again?” – the multiple expands violently. Shorts cover. Growth investors reenter. Retail piles in. And the company, now leaner and smarter, starts actually printing better numbers.

That’s what happened with Carvana. And we’re watching the early innings of that same movie with Opendoor right now.

The stock’s up 10x in 20 days. But if the story holds, it could soon turn out that this is all just the trailer.

Narrative Reversal Could Send Opendoor Even Higher

If you’re thinking that Opendoor’s rally is just a meme-fueled fluke, you might be missing the bigger picture.

This isn’t GameStop, AMC, or Bed Bath & Beyond.

This is Carvana 2.0 – an AI-enabled, tech-powered disruptor that got crushed by the cycle, adapted to survive, and is now poised to thrive in a stronger economy.

Bet against it if you want. But don’t be surprised if $5 turns into $50…

Because this might just be Opendoor’s big moment.

And it may only be the beginning.

AI helped Opendoor rewrite its future. But real estate isn’t the only industry on the cusp of disruption…

Because the same technology that’s powering smarter home valuations could soon reshape the global labor market.

We’re talking about humanoid robots: AI-driven machines designed to walk, talk, and work like us.

Tesla (TSLA), Figure AI, and others are racing to perfect them. And if they succeed, it could unlock a trillion-dollar transformation.

Want to know which companies are best positioned to ride this wave?

Find out about the firms poised to pop before Wall Street catches on.

P.S. Over at TradeSmith, Keith Kaplan just revealed the biggest predictive breakthrough of his career: a data-driven system that’s nailed dozens of stock surges with 83% accuracy.

His “Green Day” method has already uncovered six double-your-money trades this year… and it’s flashing again right now. Watch that free event – and see which two stocks to target next.