The VCX Frenzy Is a Warning for AI IPO Investors

It started as one of the most electric market debuts in recent memory. On March 19, the Fundrise Innovation Fund (VCX) – a single, publicly traded security wrapping Anthropic, OpenAI, and SpaceX – listed on the NYSE and promptly went haywire. Within four trading sessions, shares surged 1,740%, from $31.25 to an intraday high of $575. Circuit breakers fired. Trading halts were called on back-to-back days. At its peak, investors were paying more than 30 times the actual value of the assets inside the fund.

Then came Citron.

On March 26, Andrew Left’s activist short-selling firm posted on X with a simple message and a chart titled “VCX Explodes!” – and within minutes, the stock plummeted from over $400 to around $270 as 31,000 shares changed hands. By the close, shares had fallen 49%. The fund that retail investors had rushed into as their ticket to the AI revolution had just been cut nearly in half in a single session.

As of this writing, VCX trades at around $130 – a roughly 585% premium to the actual value of its underlying assets. The mania isn’t over. But the easy part of the trade is.

We’re publishing this on April 1. None of it is a joke. And the most important part of the story is still ahead.

Inside the AI IPO Pipeline: Anthropic, OpenAI, SpaceX

Nobody pays 30 times the value of something unless they desperately want what’s inside. So what’s inside?

VCX’s largest holding is Anthropic – one of the most important AI companies in the world. Indeed, by many accounts, it’s built the best frontier model available today. And the company’s revenue trajectory is simply historic: from roughly $1 billion annualized at the start of 2025 to a $14 billion run rate by early 2026. It closed a $30 billion Series G in February 2026 at a $380 billion valuation, has hired IPO counsel, and is widely expected to file for a public listing before the year’s end. When it does, it will almost certainly be one of the most significant market events in a generation.

Then there’s OpenAI, the company that started the entire AI Boom. The ChatGPT creator put generative AI on the cultural map and permanently changed what consumers and enterprises expect from software. Its latest financing round values it north of $840 billion, and it is targeting a potential IPO valuation of $1 trillion. That would make it, at debut, one of the most valuable companies in American history.

And among its smaller – but no less significant – holdings is SpaceX: widely considered the most valuable private company in the world. Its Starlink satellite internet network serves millions of subscribers across 155 countries. Its Falcon 9 rocket handles more than half of all orbital launches on Earth. The company filed confidential IPO documents with the SEC earlier this month and is targeting a June 2026 listing at a valuation between $1.5- and $1.75 trillion – a figure that would make its IPO the largest in history by a wide margin, dwarfing even Saudi Aramco‘s record $29.4 billion offering.

VCX owns all three companies – before they’ve gone public – through a single, liquid, exchange-traded security that any retail investor can buy with a brokerage account. No wonder the market was going bonkers for it.

But there’s a big difference between something being conceptually understandable and being financially rational.

The Math Behind VCX’s Premium Problem

At the time of its listing, VCX’s net asset value (NAV) was $18.97 per share. Within four trading days, it reached an intraday high of $575 – more than 30 times the actual value of its underlying assets.

Now, as of this writing, the fund trades around $130.

The reason for this sharp decline? The structure couldn’t support the price.

At its peak, investors weren’t just buying exposure to Anthropic, OpenAI, and SpaceX. They were paying an extreme premium for access – access that only exists as long as those companies remain private.

That distinction matters more than any valuation model – because the moment that access becomes widely available, the premium collapses.

That’s VCX’s core flaw. The trade hinges less on whether these companies succeed and more on how long they remain out of reach.

Walk through the mechanics. VCX owns minority stakes in a handful of elite private companies. The appeal is straightforward: you can’t buy Anthropic directly, so you buy the closest proxy. In the early days post-listing, that scarcity pushed shares to extraordinary levels.

But scarcity fades. Liquidity doesn’t.

When these companies eventually IPO, the rationale for paying a premium quickly erodes. Investors are no longer buying access. They’re holding a fund that owns what can now be purchased directly – without the markup.

As the underlying companies succeed, the fund’s advantage compresses.

This is a trade where success becomes the exit signal.

There’s also the supply side. Most of VCX’s pre-IPO investors are locked in at entry prices around $19 per share. When that lockup expires and that large base of holders can sell into the public markets, the supply shock will be severe. That kind of overhang doesn’t require a narrative shift, only an opportunity.

What’s playing out now is a transition.

VCX is moving from a narrative-driven asset – priced on scarcity and excitement – to a financial asset, where price has to reconcile with net asset value, liquidity, and supply.

Assets in that phase rarely sustain extreme premiums.

Smarter Ways to Invest In the AI IPO Wave

Gaining exposure to the most important private AI companies before they go public is a powerful strategy. But there are other ways to access the same core exposure without paying for a premium that disappears as soon as the story delivers.

Three of them stand out right now.

SuRo Capital: AI IPO Exposure at a Discount

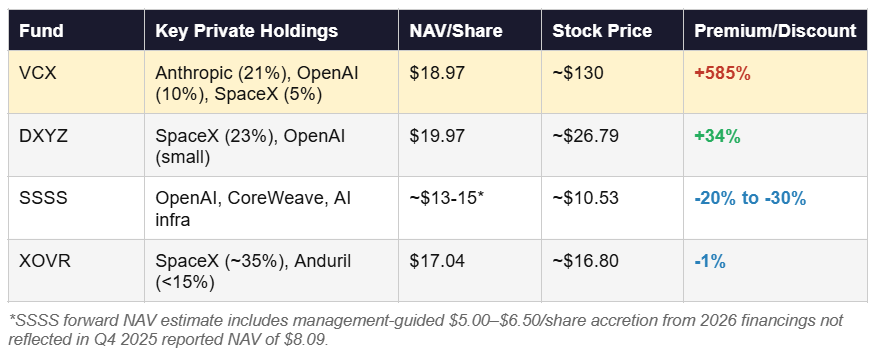

SuRo Capital (SSSS) is the original publicly traded venture fund. Its portfolio spans approximately 35 private technology companies, with a heavy emphasis on AI infrastructure. Key holdings include OpenAI, which SuRo has held since the company was a fraction of its current valuation, as well as a significant CoreWeave (CRWV) position that generated meaningful realized gains when the firm went public in 2025.

SuRo reported a Q4 2025 NAV of $8.09 per share. However, on its March 2026 earnings call, management disclosed that 2026 financings not yet reflected in the year-end marks – including OpenAI’s latest massive financing round – are expected to add between $5.00 and $6.50 per share to NAV. That implies a true forward NAV of $13 to $15 per share. SSSS currently trades around $9.89.

Put that together, and you have a fund with significant OpenAI exposure trading at an implied 25% to 30% discount to its forward NAV.

In a world where people are paying 585% premiums next door, SSSS is offering AI mega-IPO exposure at a discount.

Destiny Tech100: A More Rational Premium

Destiny Tech100 (DXYZ) is the most direct comparable to VCX in terms of structure – a pure closed-end fund holding only private companies, with no public equity sleeve diluting the exposure. Its portfolio of approximately 24 companies is anchored by SpaceX at roughly 23% of assets, with smaller positions in OpenAI and, more recently, Anthropic after a post-year-end investment.

DXYZ reported a Q4 2025 NAV of $19.97 per share. The stock currently trades around $26.52 – a 33% premium to NAV. That premium reflects a rational market assessment of the scarcity value of holding a liquid vehicle with SpaceX and OpenAI exposure. It is elevated, yes; but it is the kind of premium you’d expect for a unique product offering hard-to-access assets.

Thirty-three percent versus 585%…

XOVR ETF: Diversified AI IPO Exposure

ERShares Private-Public Crossover ETF (XOVR) takes a different structural approach.

Rather than holding only private companies, it combines a public equity core – tracking ERShares’ proprietary Entrepreneur 30 Index – with a measured private equity sleeve capped at 15% of assets. Current private holdings include SpaceX – held through an SPV and representing a meaningful share of the fund’s private equity sleeve – and Anduril Industries, the defense technology company building AI-powered autonomous systems for the U.S. military.

XOVR’s NAV sits at $17.04, while the stock currently trades around $16.80, as of this writing. With XOVR, investors are buying SpaceX and Anduril pre-IPO exposure at a discount to the fund’s stated asset value, packaged alongside a diversified basket of publicly traded large-cap innovators. This is as close to a free lunch as you’re likely to find in this space.

The tradeoff: because more than 85% of XOVR is in public equities, the private-company kicker is diluted. But for investors who want a measured, ETF-structured exposure to the pre-IPO AI and defense wave without taking on the concentrated risk of a pure-play VC fund, XOVR offers a uniquely clean on-ramp.

The Comparison You Need to See

The Bottom Line On the AI IPO Trade

The VCX craze is a masterclass in what happens when genuine excitement about transformative technology collides with a microscopic float and an army of retail investors armed with Robinhood accounts.

We think the underlying thesis – that Anthropic, OpenAI, and SpaceX are going to be among the most valuable companies in human history – is probably correct. The execution of expressing that thesis through VCX at a hefty premium is not.

The good news is that the AI mega-IPO story is real, the opportunity is enormous, and there are rational ways to participate.

SSSS, DXYZ, XOVR – none of these are perfect instruments. All carry the standard risks of pre-IPO investing: illiquidity, valuation uncertainty, lockup provisions, and the ever-present possibility that the underlying companies’ IPOs are delayed, dilutive, or priced in ways that disappoint.

Yet all three are far more rational than paying $130-plus for $19 worth of assets.

The AI mega-IPO wave is coming. But you don’t need to lose your mind – or your capital – to ride it.

And if you want to go even further upstream than SSSS, DXYZ, or XOVR, we’ve found a way for everyday investors to stake a claim in OpenAI itself before it ever trades on a public exchange – for under $10.

The biggest gains in market history haven’t gone to investors who bought on IPO day. They’ve gone to those who were already inside when the doors opened. That window is still open – but it won’t be for long.

Here’s how to be early on OpenAI.